How to plan for retirement is an important question and it’s best to start planning sooner rather than later. In this article I’ll provide an overview of some key recommendations from top sites and break it down so it is simple to follow.

Fidelity’s recommended contribution rate is to save at least 15% of your annual income

If you are able to consistently save 15% of your annual pre-tax income you’ll have a great start to reaching your retirement goals. While saving 15% is great it’s important to consider when you started and if you are consistent throughout your working years. The recommendation of saving 15% of your annual income assumes that you start saving starting at age 25 and save through age 67.

It is best to start Saving for Retirement As Early As Possible

The reason it is so important to save for retirement as early as possible is because of the power of compound interest. In summary the earlier you start to save and invest, your money will not only grow based on interest but each year the previous years interest will also grow. This will compound or increase your savings over time.

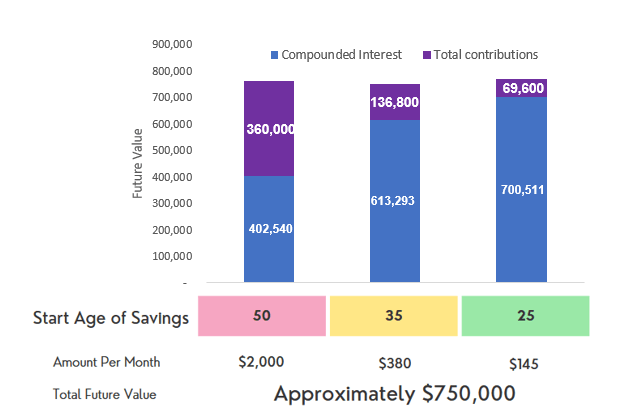

Investor.gov has a great compound interest calculator and by plugging in some savings amount by months for different ages the below graph shows how important it is start saving as soon as possible.

Assuming a retirement age of 65:

- If you start saving at 50 years old you’ll have to save $2,000 per month to have a total future value of approximately $750,000 by age 65

- If you start saving at 35 years old you’ll have to save $380 per month to have a total future value of approximately $750,000 by age 65

- If you start saving at 25 years old you’ll have to save $145 per month to have a total future value of approximately $750,000 by age 65

If you start later it is certainly possible to have enough to save for retirement you just have to be more aggressive in the amount you save or adjust your lifestyle accordingly.

Better Understand your Retirement Goals as the Amount of Savings Required For You Could Vary

While a general rule of thumb is to save approximately 15% of your pre-tax income for retirement the actual amount for your situation could vary upon the below factors:

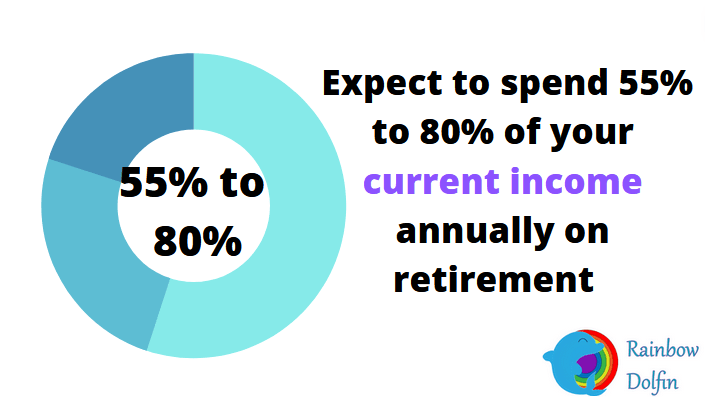

- How much you expect to spend in retirement?

- What part of the country you plan to live in?

- What type of lifestyle do you plan to live? For example do you expect to travel and eat out a lot?

- Will you have to continue mortgage payments or have other significant expenses in retirement?

- When do you plan on retiring?

If you plan to travel a lot and live in a high cost area for example you’ll want to plan for 80% or more of your current income for retirement.

Source: Fidelity.com

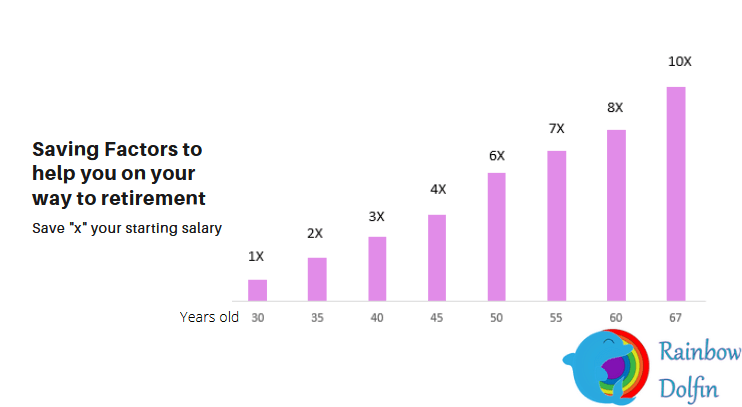

General Rule of Thumb Savings by Age: Are you on Track?

Fidelity also has a recommendation of how many times your annual salary you should have saved to see if you are on track. This is a helpful general guidance to see if you are on track or should be more aggressive in your savings.

Source: Fidelity.com

Retirement savings factors are hypothetical illustrations, do not reflect actual investment results or actual lifetime income, and are not guarantees of future results. Targets do not take into consideration the specific situation of any particular user, the composition of any particular account, or any particular investment or investment strategy. Individual users may need to save more or less than the savings target displayed depending on their inputs retirement age, life expectancy, market conditions, desired retirement lifestyle, and other factors.

What If You didn’t start Early Enough? You Can Make Adjustments

If you didn’t start saving for retirement early enough or if you had to decrease your savings due to stopping working (taking care of kids, etc.) there are ways to make up for retirement contributions. Some options are included below:

- Increase your savings percentage to more than 15%

- Increase your income by starting a side hustle or asking for a raise

- Consider decreasing your retirement costs by relocating to a cheaper area

- Continue working longer than planned

I ended up taking one year off after my first son was born and during the birth of my second son. For me it was important to take time off and to make up for the lost savings I have been more focused on savings and earning after I went back to work. I have been consistently savings and investing in my 401(k) since after my second son was born or for over the past seven years.

There are always options to ensure you have a successful retirement as long as you plan accordingly and are willing to put in the hard work and make sacrifices if necessary. Planning for retirement is a long term commitment and it is okay to adjust as life events occur.

You can always make adjustments to your plan and should check back on your plans frequently (at least once a year) to make sure you are on track.

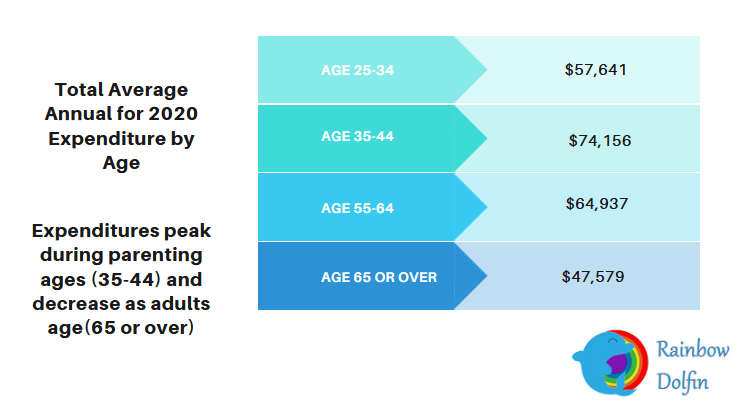

Expenditures on Average Decrease After 65+

To help with determining the approximate annual expenditures you may require annually the below chart shows the average annual expenditures by age for 2020. As you can see expenses increase from age 25-34 to age 35-44. This is likely due to parents taking care of their children and the resulting increased costs, then as their children become more independent average annual expenditures decrease slightly from ages 55-65. Then expenditures decrease again age 65 or over which is partially due to lower housing costs from older adults downsizing their homes or paying off their mortgages.

This should give you an idea of how your expenses may change over your lifetime and should help you in planning for retirement.

Source: United States Department of Labor BLS Data Labs

Invest Savings in 401(k) or Another Tax Efficient Investment

What is a 401(k)?

A 401(k) is a company sponsored retirement account where employees contribute income and employers can provide a matching contribution. Most companies provide a 401(k) which means the employee can select a certain percentage to automatically withdraw from their paycheck and it will be automatically included in the company sponsored 401(k) account.

Pros to a 401(k):

- The contributions to the 401(k) are automatic based on the percentage or dollar amount the employee selects. This means you don’t have to think about transferring the money monthly and the money never touches your checking account thus you are less likely to spend it.

- There are tax savings on 401(k) depending on which type 401(k) is selected. See below for the difference between a traditional 401(k) and a Roth IRA.

- Some employers will have a matching program where they will match up to a certain percentage of each employees income. This can typically range between 2% to 6% of the employees income. For example for an employee making $100,000 an employer would match up to $4,000 for the year if matching at 4%. So if the employee contributed $10,000 to their 401(k) for the year their employer would contribute another $4,000, having the total contributions be $14,000 including both the employee and employer portion. This is an excellent benefit to take advantage of if you employer provides matching.

Cons to a 401(k):

- There are management fees associated with your employers 401(k). So if you are looking for a low expense ratio of an index fund for example this may not be available. Be sure to look at fees closely. In general it is better to have the management fees be below 1% per year. In fact, I strive for closer to 0.5% or less per year.

- There are typically limited options of funds to invest based on what your employers selects. Typically the options include a targeted age portfolio that adjusts investments based on your targeted retirement date. For example if you plan to retire in 2040 you can select a 2040 fund which will have more aggressive stock selections as you are further from retirement and more conservative investment selections the closer you get to reaching retirement age such as bonds.

- There is typically a 10% penalty for withdrawals before the age of 59 1/2 unless you are able to meet the qualifications for an IRS hardship withdrawal.

Traditional 401(k):

- Pre-tax employee elective contributions are made with before-tax dollars. As the contributions are made with before-tax dollars you are not taxed on the contributions. For example if you make $5,000 per month and you are contributing $1,000 per month to your 401(k) then you are only taxed on $4,000 and not the contribution to your 401(k) at the time of contribution. You will be taxed at the time of withdrawal (ie at retirement).

- Additionally there is no income limitation to participate.

- It is very important to note that the combined contributions for an individual between the traditional 401(k) and Roth IRA cannot exceed $20,500 for 2022. This means that if you only invest in a traditional 401(k) your contribution cannot exceed $20,500 for the year. Alternatively if you contribute to both a Roth IRA and traditional 401(k) your combined contributions cannot exceed $20,500 for 2022. As such you should very closely calculate how much you contribute for the year to make sure you don’t exceed this amount especially if you are a high income earner.

Roth IRA:

- Roth IRA contributions are made with after-tax dollars. As contributions are made after-tax you are taxed on the contributions. For example if you are making the same $5,000 as the example above and you contribute $1,000 to your Roth IRA then you are taxed on the entire $5,000. So if your tax rate is 30% for example then you will owe $1,500 in taxes for that month. Additionally if you make more than modified Adjusted Gross Income limits (married limit of $214,000 or single limit of $144,000) then you cannot contribute.

- Contributions are limited to $6,000 plus an additional $1,000 for employees age 50 or over in 2021 and 2022.

For me personally I have been contributing pretty regularly to a traditional 401(k) and try to maximize my contributions up to the IRS limit each year (for 2022 it is $20,500).

Pro Tip: At a minimum max out your employer 401(k) match if one is provided.

Leverage Both 401(k) and Other Investments to Save for Retirement

It is much better to save and invest too much for retirement than not enough. While it is great to have a 401(k) it is also smart to be able to leverage other investments. For example in addition to my 401(k) I also have significant investments in index funds. This should allow me to balance withdrawals from both my 401(k) and my regular brokerage accounts.

By being able to withdraw from both my 401(k) and my regular brokerage accounts this will allow me to reduce my taxable income in retirement as my taxable income from my regular brokerage accounts would be taxed based on capital gains tax which is currently 20%. In addition, in case I end up retiring early than 59 1/2 either by choice or because for some reason I am not able to continue working having funds in both types of accounts allows me flexibility especially as withdrawing from a 401(k) account can have a 10% penalty.

Pro Tip: Prioritize Saving for Retirement and Save and Invest as much as you can

Conclusion

In conclusion if you take the below steps for planning for retirement you should be well on your way to having a successful retirement.

- Strive to save at least 15% of your income

- Start saving for retirement as early as possible

- Better understand your retirement goals so you’ll know how much to save

- Determine if you are on track for saving for retirement

- Make adjustments in case you did not start saving early enough

- Invest in both a 401(k) and other investments to allow for flexibility during retirement

What are you retirement goals? Are you on track? What are your strategies to stay on track for retirement? Would love to hear your feedback if the article was helpful. Thank you reading!

1 thought on “How to Plan for Retirement?”